I’m writing this article for those of you that are either curious or unsure of your ability to qualify for a conventional home loan.

Lenders will sometimes impose additional requirements, making it harder to qualify. If you need an exception that can be found below, but your current lender or mortgage broker isn’t offering it, please contact me for help.

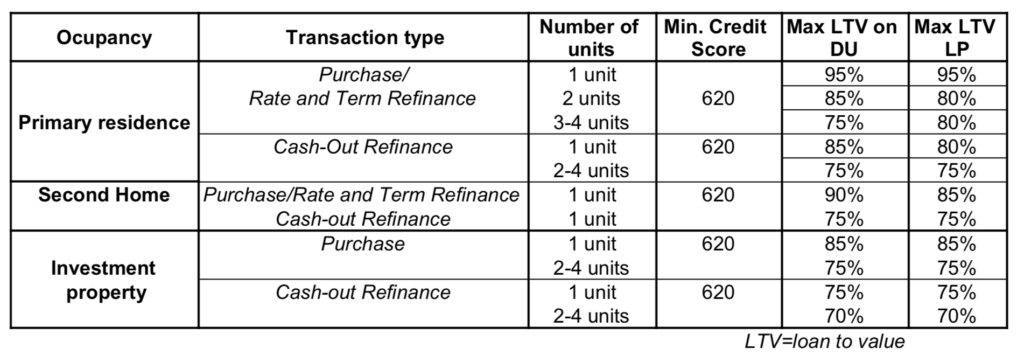

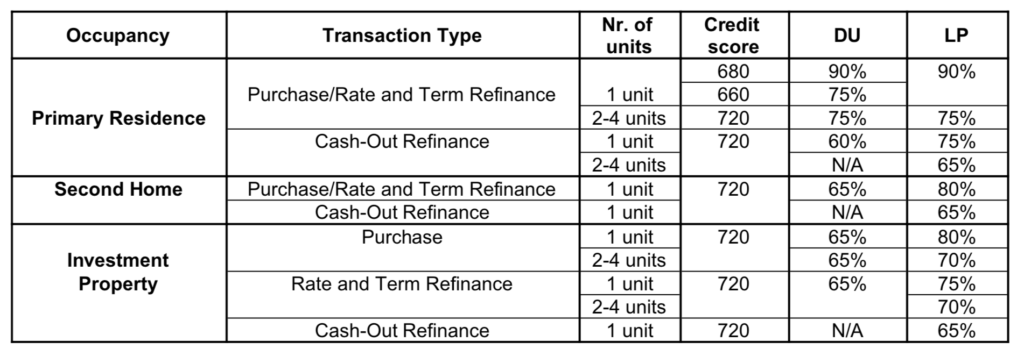

Definitions: If you’ve ever heard the terms Conventional and Conforming thrown around, here is a brief explanation:

Conventional loans are not issued or guaranteed by the U.S. Government, but rather by private lenders. They are loans that require private mortgage insurance unless you have a 20% down payment – the private mortgage insurance covers anything over the 80% that the lender is putting at risk by giving you the loan.

The following article summarizes, simplifies, and generalizes most lenders’ guidelines for approving a mortgage application in Utah

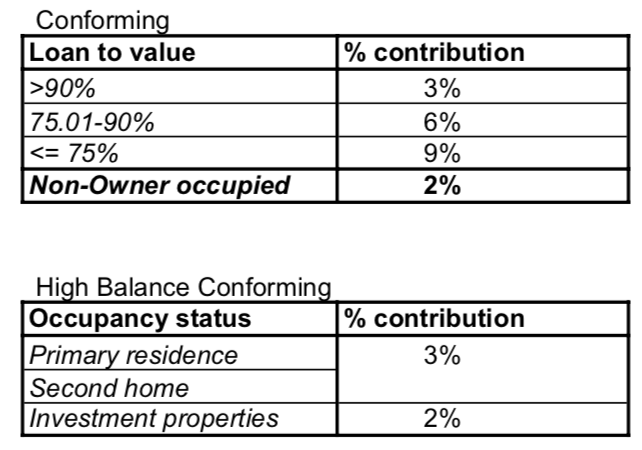

A Conventional loan that conforms to certain loan amount limits is considered a conforming loan.

Lenders sell conforming, eligible loans to Fannie Mae and Freddie Mac whenever they need to replenish their cash reserves – this is known as the secondary market.

Below is a table showing the maximum 2023 conforming limits for Utah mortgage loans, dependent on County location: